The bottom line

Peaking economic indicators suggest that we are entering a new phase of slowing momentum and a more moderate Fed response.

With growth and inflation easing, rate volatility could moderate, and Treasuries could regain some effectiveness as a hedge.

We favour high-quality fixed income assets that could weather economic volatility and provide attractive yields.

A synchronized slowing

We believe a rare macroeconomic alignment is underway in the US and other major economies: synchronous peaks in labour market tightness, industrial production growth, and inflation. Financial market performance and central bank actions in 2023 will be shaped by how fast these indicators fall.

All three indicators in question are cyclical, but their cycles differ. In the past forty years, US industrial production growth has had many clear peaks (Chart 1), but unemployment turned sharply higher only during the recessions, which occurred on average once per decade (Chart 2).

Chart 1: Industrial production cycle is near peak

Source: BlackRock, Haver Analytics as of 6 January 2023.

Peaking economic indicators suggest that we are entering a new phase of slowing momentum and more moderate Fed response.

Chart 2: Tight jobs market is losing momentum

Source: BlackRock, Haver Analytics as of 6 January 2023.

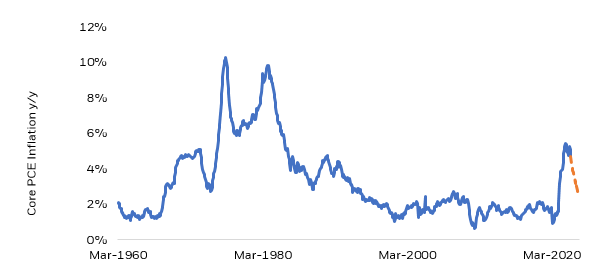

Core inflation had a clear and high peak in 1982, but since then there have been no episodes similar to the decline that forecasters now expect. Industrial production could slow as interest sensitive spending on business investment, construction, and durable consumer goods will be hampered by tight monetary policy and slowing job growth. The alleviation of certain pandemic supply shortfalls has helped manufacturing activity recently, but in 2023 gluts could replace shortages in some industries.

Chart 3: We see a core inflation slowdown ahead

Source: BlackRock, Haver Analytics as of 6 January 2023. BlackRock forecast starting December 2022. Forecasts are based on estimates and assumptions. There is no guarantee that they will be achieved.

Translation to inflation: an imprecise art

Although we expect the pace of inflation to ease, manufacturing weakness alone may probably not be enough to sustainably return inflation to low levels. The Federal Reserve is seeking to reduce inflation by creating slack by seeking to drive the unemployment rate up via restrictive monetary policy. How far it goes will determine the severity of the growth slowdown. But because uptrends in unemployment are strongly associated with recessions, any sustained increase will be very important for financial markets.

The combination of supply side healing, slowing manufacturing growth, and a weakening labour market, should all work to lower inflation. Inflation continues to confound central banks’ forecasts, so just like with unemployment, it is the extent of the change, not the direction, that financial markets are trying to determine.

Three peaks: a solid story for fixed income

Slower manufacturing activity, rising unemployment, and falling inflation all tend to lead to a decline in interest rates historically, and the “triple peaks” backdrop likely caps how much yields could rise further. Although we continue to see the Fed hiking the policy rate to around 5% in early 2023, we anticipate a potentially lengthy pause as the Fed attempts to engineer a soft landing while assessing the lagged impact of previous tightening.

As markets digest what we think will be the increasingly visible slowdown in growth and inflation, this could provide a tailwind for fixed income assets. Within the space, we continue to focus on up-in-quality exposures such as high-quality investment grade assets and agency mortgages that could weather economic volatility while providing attractive yields (Chart 4).

Chart 4: High-quality fixed income yields

Source: Bloomberg as of 6 January 2023. Bloomberg indices utilised: “10y Treasury Yield” = USGG10YR Index, “10y Real Yield” = GTII10 Govt, “US IG Yield” = BUC1TRUU Index, “US MBS Yield” = LUMSTRUU Index, “US Aggregate Yield” = LBUSYW Index. Indices are unmanaged and one cannot invest directly in an index. Past performance does not guarantee future returns.

Looking ahead, this rare “three peaks” scenario could create an environment that has not been seen in years, namely a generational inflection point in financial markets. We see the following implications:

Rate volatility could moderate, a key condition for solid fixed income returns: In this scenario, interest rate volatility could decline from historically elevated levels. This means fixed income assets could be poised for a multi-year runway for the potential to generate strong returns. While there are still many unknowns, this triple peak scenario also raises opportunities for active managers who may judge correctly the extent of adjustment that will occur.

Treasuries may be an increasingly important source of diversification and volatility dampening: At current valuations, in a severe growth shock we believe US Treasuries will regain some effectiveness as a hedge to riskier products in portfolios. This contrasts sharply with the lack of diversification provided by the sector in 2020-22.

Access more insights from BlackRock.